It’s the end of the year. What have we spent all of this time talking about?

Mostly what it means that pension funds, sovereign funds, endowments, and other asset owner institutions collectively manage roughly a third of all the money on earth.

They tend to be globally diversified and invest with long time horizons, which aligns them with the public interest because they cannot succeed unless human enterprise flourishes around the world. They also provide most of the world’s risk capital, which makes them the base of modern capitalism.

Our mission at Free Money is to help them find the freedom to properly fulfill their potential, orient their operations toward projects that build collective value, and serve as truly effective stewards of society’s accumulated capital.

It’s more profitable to try and extract value from them, so we have plenty of competition. But our greatest enemy is ignorance, not malevolence. So we spent the last episode of the year talking about at least five forces which work together to leave the world’s financial plumbing in thrall to the tyranny of low expectations.

We’ll enumerate and examine each in essay form after this quick word from our sponsor.

Are you aggravated by average? Obsessed with outperforming ordinary? Tired of what's typical?

You're not alone. Most investors expect exemplary experiences, but reality seldom satisfies. That doesn't have to be true for you! Free Money is pleased to introduce Portable Alpha, a revolutionary sports drink with a propriety mix of caffeine, taurine, and orange.

Future profits* are assured once we've given you permission to order, and the first serving is free! It will be shipped in a black box with only a few additional fees once you order an additional 127 servings. You'll start performing abnormally once it hits your lips.

The global supply of Portable Alpha is limited, and Free Money is its exclusive distribution agent. Don't miss your chance to buy it! Click here to sign up for the Free Money email list today.

*Profits will accrue to Free Money Holdings, a Cayman Islands limited liability company. The Influence of Unexamined Norms

Substantially every form of diversity imaginable is present among institutional investors. They exist in China, California, Canada, Texas, Taiwan, and Tuvalu. Some invest to support educational institutions while others provide insurance or fund members of a certain family. At least one is meant to stabilize the country of Iran.

With so much inherent difference, we wonder: why do they act so similarly?

One reason is that they have constraints which vary in their specifics but create similar operating conditions. For instance, they often hold monopolies over the assets they manage, which creates incentives for staff to optimize for not getting fired, rather than what’s best for the organization.

On top of that, conformity tends to be written into the law in the form of the prudent person rule, which states:

A fiduciary must discharge his or her duties with the care, skill, prudence and diligence that a prudent person acting in a like capacity would use in the conduct of an enterprise of like character and aims.

On the surface, this makes a lot of sense. Skill, prudence, and diligence clearly belong inside of an investment decision-making process.

But imagine trying to apply investment skill while required to mimic a person acting “in a like capacity” at “an enterprise of like character and aims.” What if you are able to recognize and access opportunities that your peer group can’t imagine? Are you to forego such opportunities and thereby constrain your ability to access abnormal returns?

It does not pay to ask such questions in investment committee meetings, which exist to pursue and monitor certain prescribed forms of commerciality. The lie that these normative constraints on capital allocation are innate to all sound investing processes thus impairs every asset owner institution, effectively constraining all capitalist processes by misaligning the risk capital that serves as their feed stock.

Recognizing the existence of this lie does not naturally render investment decisions it affects incomplete or invalid, simply influenced by an unacknowledged force altogether different from the “invisible hand” of a “free market” which neither executive leaders nor board-level overseers often contemplate or choose to engage with. Instead, market participants are blinded to alternative investing styles in much the same way that most adults were blinded to queer lifestyles before recent increases in lesbian, gay, bisexual, and transgender visibility.

The Pleasant Fiction of Free Markets

Unlike normative forces, the influence of market forces has been contemplated extensively. Much of this literature makes the case that something called a “free market” determines which goods are bought and sold and the prices at which those transactions take place.

Leonard E. Read’s essay I, Pencil is a representative entry in this literature. In it, Read tells the story of a simple lead pencil, tracing the many people, processes, and places that play a role in its construction. The pencil itself is presented as a miracle of the market, since it came into being even though no one person in its complex supply chain possesses all the requisite knowledge to make it from scratch.

Read then contrasts the process which birthed his marvelous pencil with the machinations of government, arguing that any government program inhibits creative energy and introduces unnecessary costs on human enterprise.

We prefer pens, but agree with Read that the large-scale cooperation required to construct a pencil is pretty cool. However, his assertion that it takes place in a marketplace untouched by government action is categorically false. 34 of of the 50 largest pensions in the United States are linked to government entities, meaning that the pencil factory that serves as the site of his miracle may well be bankrolled by the very same government he wrote the essay to denounce.

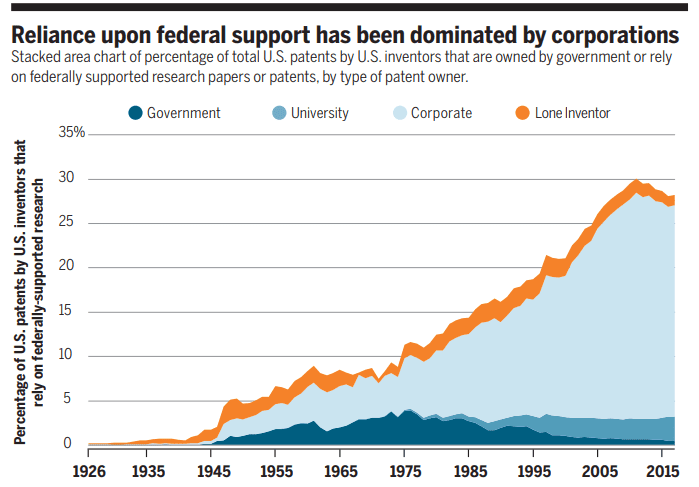

In fact, government funding fuels an increasing share of basic innovation in the United States. The chart below—published in the peer-reviewed journal Science—shows that more than a quarter of U.S. Patents relied on federally supported research, and that corporations are the largest beneficiaries of this support.

One would hope that the government’s track record spoke for itself after funding the research which led to GPS, airbags, cellular phones, lithium batteries, and the internet. Most traditional investors would have had a hard time funding the long-term fundamental work which birthed each of these technologies since the outcomes of such efforts are inherently unclear.

With that said, these investments in basic research are crucial, and we believe society should be organizing itself to make more of them. Whether it’s concentrated on curing disease or alleviating the effects of climate change, the government can clearly be an effective supporter of curiosity and creator of capitalist opportunity.

Individually Rational, Collectively Insane Actions

To estimate the costs associated with the unstudied norms we discuss in section 1, take a look at the chart in section 2. It should be surprising that corporations own so many of the patents generated by government research, but it probably isn’t to most readers.

If asset owners were able to take fuller advantage of unconventional opportunities, it’s likely that this chart would look a little different. Think about it: much of this research work takes place at universities, which typically also have endowments. The people pursuing promising cutting-edge research may share a dining hall with the investors tasked with finding compelling investment opportunities.

Why not invest where they eat?

Some sophisticated university endowments might already, but for many staff such a suggestion smacks of career risk. If the investment went wrong or simply under performed, they’d face scrutiny and perhaps consequences. So private corporations capture the rewards of this public spending instead.

If this were the only individually rational, collectively insane behavior in the financial markets, it might not be such a big deal. But it’s far from isolated. At one time, it would have been safe to assume that the corporation that eventually patented these new technologies would be listed on a stock exchange. If that were the case, it would be relatively easy for an investor to share in their prosperity.

Today that’s not so much the case. There are roughly half as many listed companies today as there were in the late 1990s, and innovative growth companies are staying private longer than ever before. This means institutional investors must compete for access to illiquid, expensive investment vehicles to access opportunities that would have been readily available two decades ago.

The private equity funds that pensions pay to access previously available investment opportunities provide perfect conditions for collective insanity to flourish further. Though in some cases these firms have historically generated returns through improved governance, modern practice has moved towards more complex practices that arguably increase risk and invite significant conflicts of interest.

Roughly twenty percent of 484 healthy companies purchased by private equity funds went bankrupt within ten years of the transaction’s close. Roughly thirty-five percent of the funding for such transactions comes from public pension plans. And if recent trends are any indication, that number is only set to grow.

Institutional Resistance to Innovation

The organizations which form the base of capitalism—pensions and other asset owners—operate in government contexts. The people in charge of them are necessarily political, which compounds the difficulty of modernizing the way a given pool of capital invests.

As if it wasn’t hard enough already.

This means that although many of these enterprises would benefit from streamlining their administrative processes, the energy required to socialize and implement such reforms would be substantial. And rightly so: in many cases, people rely on these organizations to fund their daily lives. They are not the sort of environments where it’s appropriate to “move fast and break things.”

Fortunately, there are less controversial places to concentrate. There is almost a pre-built consensus for modernizing the technology that these organizations use to make investment decisions, modernize their internal administration, and communicate with beneficiaries.

Cost savings can be substantial. In Illinois, which will spend 27% of its 2020 budget on meeting pension obligations, some smaller suburban pensions incur more than $2,000 per person in administrative expenses. And that’s before considering what they pay in fees and costs to their investment managers.

Implementing new technology systems invites these organizations to evaluate and update their governance in a relatively gentle and constructive setting. It also prepares them for added scale, which can substantially reduce the cost of administration (as shown by the McKinsey chart below).

The report it comes from also indicates that a $1 billion pension fund typically pays fund managers 15% higher fees than a $10 billion fund, meaning that administrative costs aren’t the only place where plans experience increasing returns to scale. If the fund were to grow by two orders of magnitude to $100 billion, investment fees would be expected to come down by 41%.

Though the fiduciary test we discussed earlier can make paradigm-shifting innovation harder to implement, it does at least keep trustees concentrated on commercial success. This can promote myopia, but also clearly justifies investing in technology and other cost-saving measures which indirectly improve governance and increase innovation.

5. The Low Probability of Positive Change

To cynics, what we have described is an immutable characteristic of financial capitalism. In those jaundiced eyes, we’re better off hoping for faeries to magic these conditions away than believing we can build momentum for change.

After all, history does not appear to be on our side.

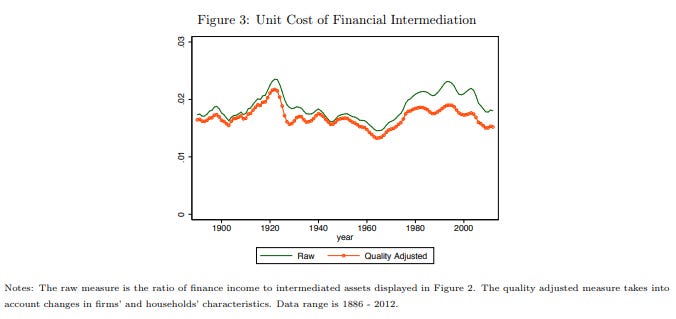

Thomas Phillipon found that despite the numerous technological advances that happened between 1886 and 2012, financial intermediaries still managed to extract a roughly constant 1.5-2% from the economy.

Why would we dare believe that anything could change?

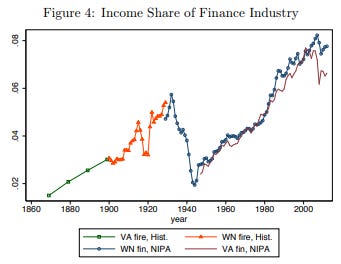

Because it already has. In the same paper, Phillipon shows that the finance industry’s share of total income in the United States has grown roughly fourfold since the end of World War II.

That’s because the country’s asset base has grown significantly while the 1.5-2% tolls that banks extract from it have remained the same. And since the industry has consistently captured this extreme amount of value for more than thirty years, we’ve almost accepted it as normal.

Almost.

Mission-oriented investors forced to pay those fees are wising up, and working together to escape them. We’ve seen asset owners direct intention towards improving their own relationships with intermediaries, reap the benefits, and invite others along the same path. That’s exciting: it means the world’s giant pools of capital are beginning to manifest their power and take charge of their own destiny. It’s happening just in time.

The threats posed by global challenges like famine, illness, and climate change cloud the future of our species. If we overcome them, it will be because society has managed to evade the strictures we describe in this essay and realign its assets to support and speed human flourishing.

Five Forces Fighting Free Money